We fix the damage and handle the paperwork your claim needs.

One company, one job.

A project manager arrives first, documents everything, and you approve the scope and price before any work starts. From there we build the file in the format insurance companies ask for — photos, moisture readings, daily logs — and meet your adjuster on site. The claim stays in your name, and you’re never on your own with it.

The repairs and the paperwork move together.

Most projects stall because the crew and the claim documentation move at different speeds. We keep our side of both on the same schedule.

- 01

Emergency response — documented from hour one

A project manager is on site within 60–90 minutes, day or night, and the free inspection starts the file: time-stamped photos of the damage exactly as we found it, before anything is moved or torn out.

- 02

Mitigation — documented as it happens

You approve the scope and price before the crew is scheduled. Once work starts: daily moisture readings, treatment logs, and photos, uploaded the same day so the paperwork never lags behind the work.

- 03

Specialty handling — kept in the same scope

If asbestos, mold, or contents work shows up mid-project, it’s scoped into the same file with its own line items. You don’t hire a second contractor or start the paperwork over.

- 04

Estimates — written the way adjusters read them

Same format, same line-item structure your insurance company uses. We negotiate our own scope and supplements in writing, and complete files remove the most common cause of delay.

- 05

Reconstruction — sequenced with adjuster approvals

Trades line up behind supplement approvals so the build doesn’t lose time waiting on the insurance side.

What we do on the insurance side, item by item.

Coverage is between you and your insurance company. Everything below is the part we own.

Help you file the claim

If you haven’t filed, we walk you through it — what your insurance company will ask, what to have ready. If you have, we make sure they get the documentation they need from us.

Documentation in the format insurance companies ask for

Time-stamped photos, moisture logs, contents inventory, signed authorizations. Complete files remove the most common cause of delay.

We meet your adjuster on site

We walk them through the damage, answer their questions, and negotiate our own scope and supplements directly. You don’t translate between four sets of people.

Scope and supplement management

When mid-job reality changes the scope, we submit the supplement in writing — before the work happens, not after.

Next-step clarity for the homeowner

You always know what stage the job is in, what’s pending approval, and what happens next. The portal makes it visible.

A scope that matches the damage

We don’t inflate to maximize claim value. Every line item is backed by a photo or a reading, and the estimate reflects what your home actually needs.

Water Damage Claims Handled the Right Way.

We work with every carrier.

These are some of the carriers Chicagoland homeowners call us about most often.

Your project manager handles the claim process with you.

EcoClean's project managers guide the job from the first water damage cleanup and dry-out through the insurance documentation and reconstruction process. We photograph the damage, take moisture readings, document the scope, and bill using specialized insurance estimating software so the claim file is organized from the start.

- Photograph the damage at arrival, before mitigation starts

- Take and log moisture readings on every affected area

- Document the scope room by room as work progresses

- Use specialized insurance estimating software for the bill

- Communicate clearly about what was found and what comes next

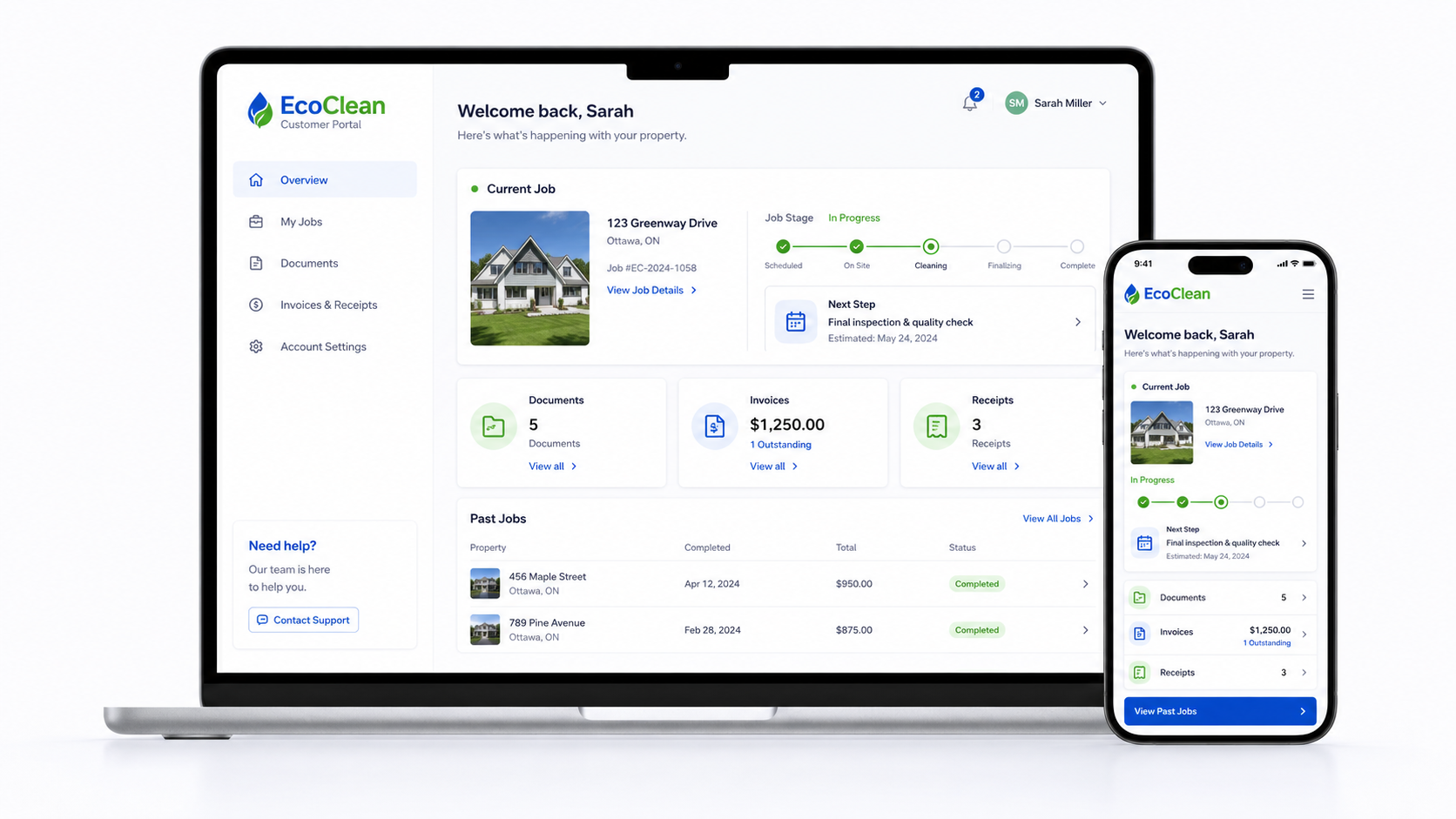

See the job, documents, photos, invoices, and packet in your portal.

Your EcoClean customer portal keeps the project organized in one place. You can see the current job status, shared documents, job photos, invoices or receipts, and download a project packet when you need everything together.

- Current job status

- Shared documents

- Job photos and media

- Invoices and receipts

- Downloadable project packet

What actually happens, in order.

- 01

The first call

You call, any hour. A project manager arrives within 60–90 minutes, documents the damage exactly as it is, and gives you a free inspection and estimate. You approve the scope and price before any work starts.

- 02

You file the claim — we help

If you haven’t filed yet, we walk you through it on the spot. The claim stays in your name; we just need the claim number and your adjuster’s contact so our documentation goes to the right desk.

- 03

Mitigation + ongoing documentation

Work proceeds while the file builds in parallel. Daily moisture readings, photos, treatment logs — all uploaded to your portal as we go.

- 04

Your adjuster reviews the file

We upload photos, moisture readings, and logs daily, so your adjuster never waits on paperwork from us. The review timeline belongs to your insurance company — complete files remove the most common cause of delay.

- 05

Estimate alignment

We negotiate our own scope and any pricing differences directly with the adjuster. Supplements submitted in writing as the project reveals more.

- 06

Repair progression

Reconstruction starts as soon as the area is dry and approvals are in place. Same team, no handoff.

- 07

Closeout

Final walkthrough, signed completion, paid receipts. Every document filed in your portal — for this job and every future job we do for you.

Things homeowners ask before they file.

Will filing a claim raise my rates?

Sometimes. That depends on your insurance company and your claim history — a single sudden loss like a burst pipe is a different conversation than several claims in a few years. We’ll tell you when filing makes financial sense and when it doesn’t, before you file.

Do I have to use the company my insurance recommends?

No. Your insurance company can suggest preferred vendors, but the choice of contractor is yours. Many of our customers come to us after trying a referred vendor that didn’t communicate well.

What if my adjuster disagrees with your scope?

We negotiate our own scope and supplements directly, with photos and moisture logs behind every line item. We’ve done this hundreds of times — most differences come down to documentation, and ours is complete.

Do I pay you, or does the insurance pay you?

With your signed authorization we can bill your insurance company directly. Checks typically go to you — and to your mortgage company if you have one — and we’ll walk you through the depreciation holdback so the payment flow has no surprises. Most homeowners never pay more than their deductible.

What if my claim gets denied?

We’ll show you why and tell you straight whether an appeal makes sense. Sometimes the loss isn’t covered and the honest answer is to pay out of pocket with a smaller scope.

Can you step in on a job you didn’t start?

Yes. If another company started the work or you’re mid-claim and stuck, we can step in. Common situation — call us.

The paperwork stops being a mystery.

Every customer gets a private portal link. The job stage, the documents, the signed authorizations, the supplements, the invoices, the photos — all there. Refresh once a day and you know everything we know.

- Current stage of the work and the paperwork

- Documents, photos, signed forms, adjuster correspondence

- Invoices and paid receipts

- Full history of every job we’ve done for you

You shouldn’t have to translate.

Whether you’re mid-claim and stuck or just starting one, we’ll walk through the damage with you and tell you straight what makes sense.